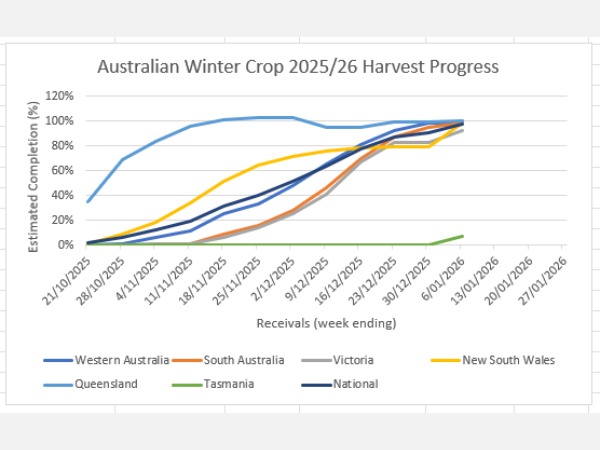

After a slow start to the Australian new crop grain export program in October 2025,…

With the Australian barley harvest finished for season 23/24, it’s a good time to review where Australia’s barley has been produced this year and assess the industry’s performance against long term averages.

Although most publications address cropping performance on a State by State basis, Australia’s barley industry in fact operates on a regional basis. The Northern region, taking in the warmer/hotter cropping areas of Northern NSW and Queensland mostly services regional feedlot demand; the Southern region takes in the temperate regions ofCentral/Southern NSW, Victoria, Tasmania and South Australia and meets domestic and export barley feed and industrial demand from the East coast and finally the Western region, which represents the State of Western Australia is a stand alone origin predominately supplying global export demand.

Although the barley crop for 23/24 fell short of reaching the incredible +13mmt national crops of the 3 previous years, it was nevertheless only the fifth time an Australian crop has exceeded 10mmt, first achieved in 2016/17. Victoria was the strongest performer against long term averages (+1mmt for barley, +400kmt for malting barley), NSW recovered from a poor 22/23 crop, particularly in Southern areas, while WA and SA were well back against their averages (collectively -900kmt for barley, -700kmt for malting barley).

Victoria and the SE more generally had ideal sowing conditions, a mild winter and although the Spring months were dry, timely rain in October restored yield potential that was mostly realized despite late rain from mid November negatively impacting crops in the Southern Wimmera and the Western district. Western Australia and South Australia were affected by the dryer Spring conditions longer than the East coast and this affected yield and malting selection, with even normally robust regions of Albury and Esperance having extremely low malting selection rates.

Digging deeper on a regional basis, whilst the South Eastern Australian contribution to the national malting barley production is normally ~30%, this year the region has produced more than 60% of the nation’s malting barley. With this, there is no doubt that the ports of Geelong, Portland and Melbourne will be a hive of activity for malting barley exports in 2024.

Related Articles